Mapping of The Ecosystem And Movement of The Chinese REE Industry

Context

We will be taking a deep analytical dive into the ecosystem and movement of light and heavy rare earths within China. Mapping and exploring all the moving parts and players of this industry and how China’s role plays out into the global light and heavy REE industry. Delving into all 3 sectors as well as logistics and shipping and the policy and regulatory environment. And within all these categories looking at domestic and international bottlenecks, inventory movements and cycles and how it plays out into the global rare earths market.

- Upstream: Mining & Extraction Ecosystem and Movement

- Midstream: Separation, Processing & Refining

- Downstream: Magnets, Components & End Use

- Regulatory Environment

- Logistics & Shipping

Executive Summary

There is a lot of noise and writings on China and the whole rare earths industry and very few have depth and insight and have mapped China and its ecosystem and its movements of light and heavy rare earths, how they move and why they move. China has managed to curate a highly effective and carefully curated ecosystem of light and heavy rare earths from mine to component in an end use application. This is lightly looked at and if mentioned, quite vague and doesn't shed light on the ins and outs of the environment in which China has carefully created over the last 60 to 70 years. In this report we delve into and map the ecosystem and movement of light and heavy rare earths operations from upstream, midstream, and downstream sectors in China including logistics and shipping and policy and regulatory environment.

We will be covering the upstream operations of both mining light and heavy operations from the different mines to where they are moved to the stage of processing and refining and the players involved. Same with midstream operations the inflow and all the processing China conducts to turn raw material into a value added product to be used. With the downstream sector we will extensively map the environment and movement within China and how it feeds out into the international markets and magnets, and components and how international markets feed in and out this ecosystem.

In regards to logistics and shipping we will be covering the shipping routes, the type of ships used and networks used by China and the rest of the world and as well as the logistical moving that happens within all 3 sectors involved in this ecosystem. And lastly we'll be looking at the backbone of this entire environment and veins that control this body, the policy and regulatory environment.

Ecosystem & Movement Market Context

It's important that we set context for the ecosystem and movement for this report with context covering key essential information that are recurring themes throughout this report and to set you up with key information for the core breakdowns of the different sectors that make up China’s rare earths industry. Lets begin with rare earth there are 2 types of REEs and they are divided into two groups:

Light Rare Earth Elements (LREEs): More abundant, with wider deposit distribution.

Heavy Rare Earth Elements (HREEs): Far scarcer, more strategically critical, and almost entirely sourced from China or within China's international operations.

Out of the two, heavy REEs are significantly scarcer and more economically valuable than light REEs. Dysprosium, Terbium, Holmium, Erbium, Thulium, Europium, Ytterbium, Yttrium, and Scandium remain the absolute choke point of the global supply chain.

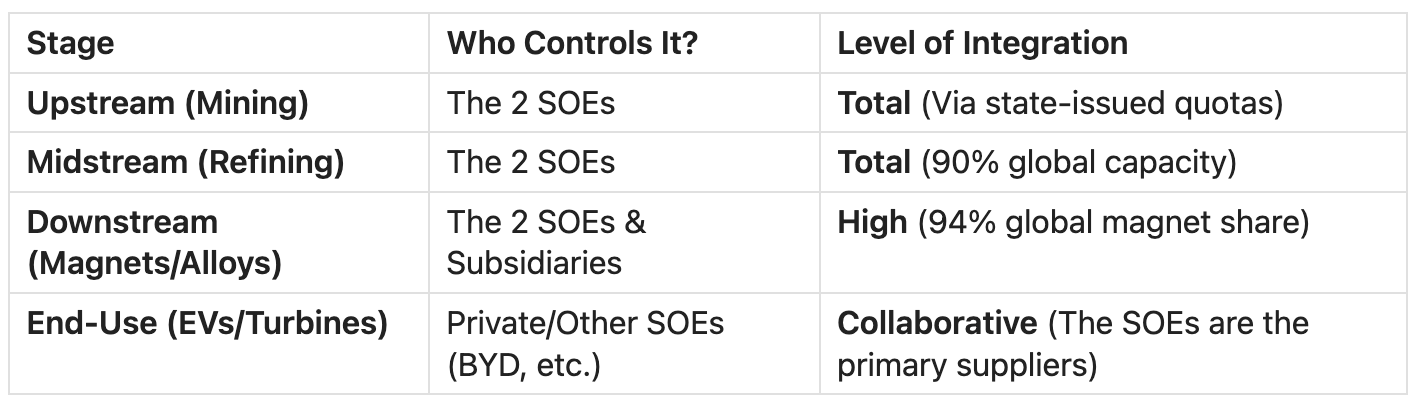

Along with being a provider China has adopted and into a strategic regulator. While the world is trying to diversify away from China's ecosystem of REE's, China still controls approximately 90% of the world’s refining and magnet production. This remains the true bottleneck even if a country mines its own ore, it likely still depends on Chinese technology or facilities to turn that ore into usable magnets and other end use applications. So they move through the Chinese supply chain either way.

China has split its domestic mining into two distinct geographic and elemental zones, controlled by two state-owned giants. Creating ecosystems in China moving from a fragmented landscape of many small miners to a state-orchestrated duopoly that controls operations domestically and internationally. Almost all movement of rare earths within China now flows mostly through two massive state-owned enterprises and their subsidiaries and a few others all connected to the Chinese state.

- China Northern Rare Earth Group: Controls the Light Rare Earths (LREEs) in the north (primarily the Bayan Obo mine).

- China Rare Earth Group: Formed to control the Heavy Rare Earths (HREEs) in the south of China and Myanmar.

China Northern Rare Earth Group (Northern China, light REE) is based in Baotou, Inner Mongolia. Its consolidation history includes:

- 2008: Merged with Baotou Steel Rare Earth, and by 2009 the combined entity commanded approximately 90% market share in key rare earth segments

- 2011: The Inner Mongolia government designated it as the sole state-controlled enterprise for rare earth mining and processing in northern China. Of 35 other regional producers, 31 were instructed to shut down and 4 private rare earth companies were directed to merge with the group

- 2012: Acquired equity in Gansu Rare Earth New Material Limited Liability Company

- 2014: Formally established as China Northern Rare Earth Group, one of China's largest rare earth corporations

The North (Light Rare Earths - LREEs):

Bayan Obo, Inner Mongolia: This is the world’s largest rare earth deposit. Managed by Baotou Steel Union who supply China Northern Rare Earth Group, it accounts for roughly 90% of China's LREE production (like Neodymium and Praseodymium).

Sichuan Province: Home to the Maoniuping mine, the second-largest LREE source in the country.

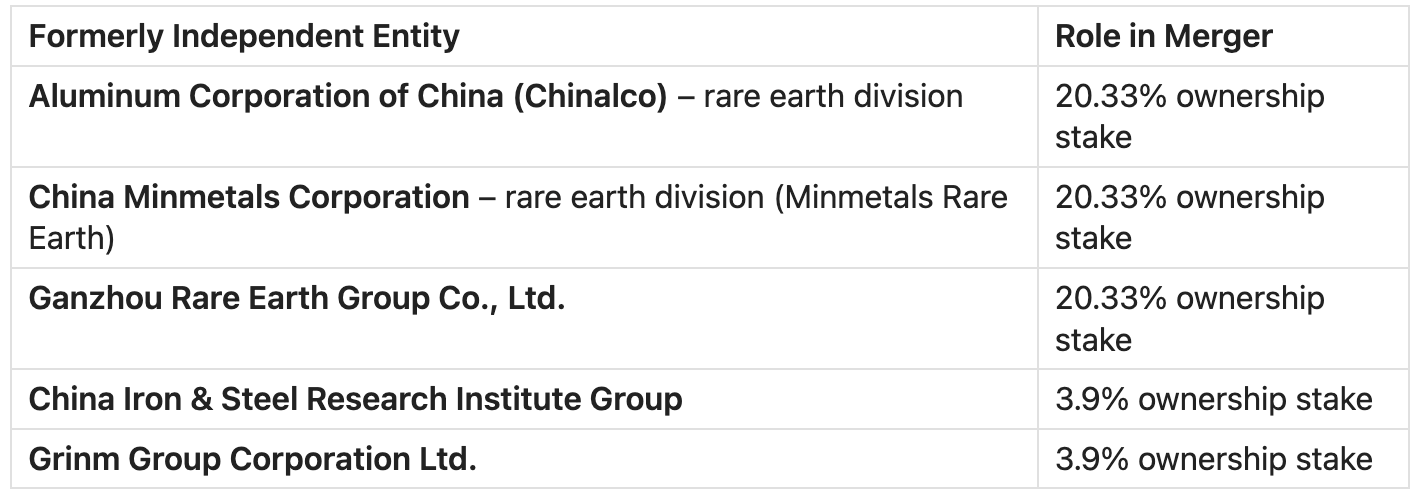

China Rare Earth Group (Southern China, Myanmar heavy REE) was established in December 2021 in Ganzhou, Jiangxi Province, this conglomerate was formed by merging three of the former "Big Six" state-owned rare earth enterprises plus two research institutes:

The South & Myanmar (Heavy Rare Earths - HREEs):

Ganzhou, Jiangxi Province: Often called the Rare Earth Capital. The ionic clay mines here provide the world’s most critical Heavy Rare Earths (Dysprosium and Terbium).

Other Southern Hubs: Mining also occurs in Guangdong, Fujian, and Hunan, primarily overseen by the China Rare Earth Group.

Myanmar: The shadow upstream Ecosystem where 50% of China’s heavy rare earths come from. China outsources the dirty mining of heavy rare earths to Myanmar in Kachin state Chipwe/Pangwa region and Bhamo District (Northern Kachin State). Where the ores moves across the border into Chinese refineries, then is legalised within the Chinese quota system, and is then moved into the global market as Chinese-processed material.

This consolidation means there is no free market for rare earths inside China. Every gram either formal or informal that is moved from a mine to a refinery is tracked by a national digital ledger, making it nearly impossible for black market or undocumented ore to leak into the global supply chain.

Alongside their domestic operations China of course has international operations going on all over the world, some examples being:

Tanzania (Ngualla) through Shenghe Resources China secured massive deposits of Neodymium and Praseodymium. |

Mexico through JL MAG Rare-Earth China establishing a magnet production site closer to the North American market (near-shoring).|

Vietnam & Brazil Strategic Investors like Shenghe Resources in Vietnam and China Nonferrous Metal Mining Group eyeing the newly discovered heavy rare earth ionic clays to expand their upstream mining and extraction ecosystem and to prevent Western-backed projects from gaining a foothold.

Continuing on with China and their international operations unlike their domestic operation where they can do as they please. In international operations there are a lot more moving parts and processes and to bypass any international pushbacks or hurdles. The two giants often use proxy companies or minority stakes to control international assets.

Let's look at Shenghe Resources as an example. While technically a semi private listed company, Shenghe is a key strategic partner (and often a proxy) for the state's rare earth goals. They hold significant stakes in:

MP Materials (USA): Shenghe was a founding investor and still holds roughly 8% stake in the Mountain Pass mine in California.

Peak Rare Earths (Tanzania): Shenghe recently moved to take a major stake and offtake agreement for the Ngualla project in 2025/2026.

Greenland Minerals: They have long held a stake in the Kvanefjeld project.

Vietnam Rare Earth Company: Holding a 90% stake in this Vietnamese mining and processing company.

Even when they don't own a foreign company 100%, the SOEs use binding off take agreements. They provide the funding for a junior miner in Africa or Australia in exchange for 100% of the raw material being sent to their Chinese refineries.

View the two SOE companies not just as producers, but as ecosystem Coordinators. They sit at the top, managing a web of hundreds of sub-companies that ensure a rare earth atom stays within the Chinese state ecosystem from the moment it is a rock until it is a motor in an EV. And any international rare earth operations inevitably flow back into the Chinese ecosystem.

It's important to note that it goes beyond owning companies and to owning the flow. Policy regulations are also a way China expands its ecosystem and control over REEs. Parent entities that now hold the exclusive rights to the most advanced processing IP. They have acquired the patents from state research institutes, making it illegal for their subsidiaries to share that tech with foreign partners. An example of this being the The 0.1% Rule new 2025/2026 regulations state that if a product made anywhere in the world contains more than 0.1% Chinese-origin rare earths by value, these SOEs (via the Ministry of Commerce) can theoretically demand oversight of where that product is sold.

Side note however in November 2025, China temporarily suspended the second wave of these export controls until November 2026, suggesting the measures remain subject to diplomatic negotiation.

Regarding the onward movement is that China no longer wants to export raw oxides. The ecosystem is designed to force the movement of rare earths downstream into finished Chinese products. It is no longer just about who owns the dirt. It is about who owns the processing patents and the magnet manufacturing. China’s 15th Five-Year Plan (2026–2030) explicitly prioritizes vertical integration controlling the journey from the mine to the final EV motor.

If a product has any sort of connection to rare earths directly or indirectly you are operating a product with strings attached to the ecosystem and movement of the Chinese rare earth supply chain.

Bottlenecks that affect rare earths ecosystem and movement

The Chinese industry has shifted from a just-in-time model to a security-of-supply model, and the ecosystem and movement in this industry that has the most bottlenecks is the Midstream, Processing and Separation and downstream Magnets and Manufacturing of end use applications.

For example, for China, the ultimate bottleneck is not production capacity, but technological sovereignty and market access. China has successfully bottlenecked the world on processing (Midstream). And their current challenge is overcoming the Western bottleneck on high-end IP (Downstream).

Another example is import dependency. Contrary to the monopoly narrative, China remains heavily import-dependent for raw mineral concentrates even with their mining & extraction scale. So to balance this out China functions as the world's refining lung, sucking in raw materials from abroad e.g., Myanmar, Australia, Tanzania and breathing out processed materials.

The bottlenecks that affect rare earths ecosystem and movement cannot be grouped and simplified because upstream, midstream, and downstream operations all have their own layers that all feed into each other on a larger scale as a whole. From structural constraints on supply flow and market tightness to inventory cycles that amplifiers of volatility through buyer behavior and policy signals that triggers the reshape flows, pricing, and investments.

To conclude, China and its 2 SOEs has set itself up from the very beginning to be the de facto ruler of the whole REEs supply chain worldwide from upstream raw material to downstream magnet manufacturing. In mining China accounts for roughly 68–70% of global rare earth mining. When it comes to processing, refining and separation China controls approximately 90% of global refining capacity. Magnet and alloy production China controls over 90% of the world's permanent magnet manufacturing.

This all a carefully curated ecosystem of operations which from top to bottom has been implemented to make sure China controls and remains at the forefront of the REE industry. So it is of most importance that we provide an in-depth and clear breakdown of this quiet yet essential ecosystem China has built and how it moves from within and how it extends into the global REE market.

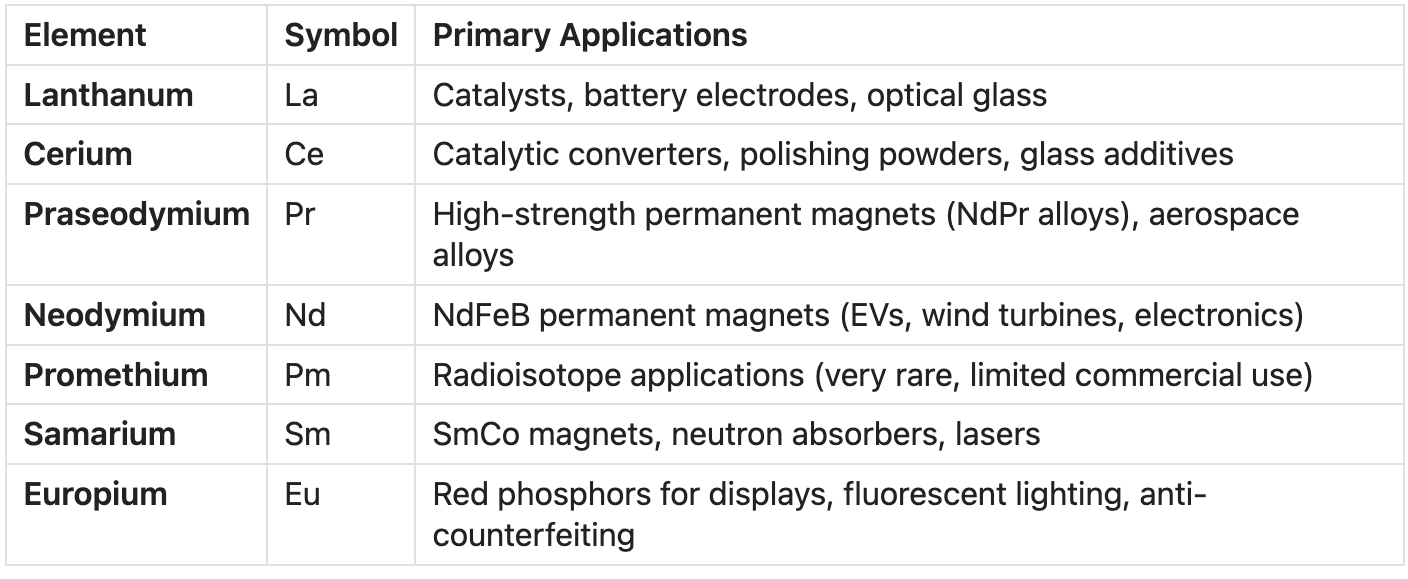

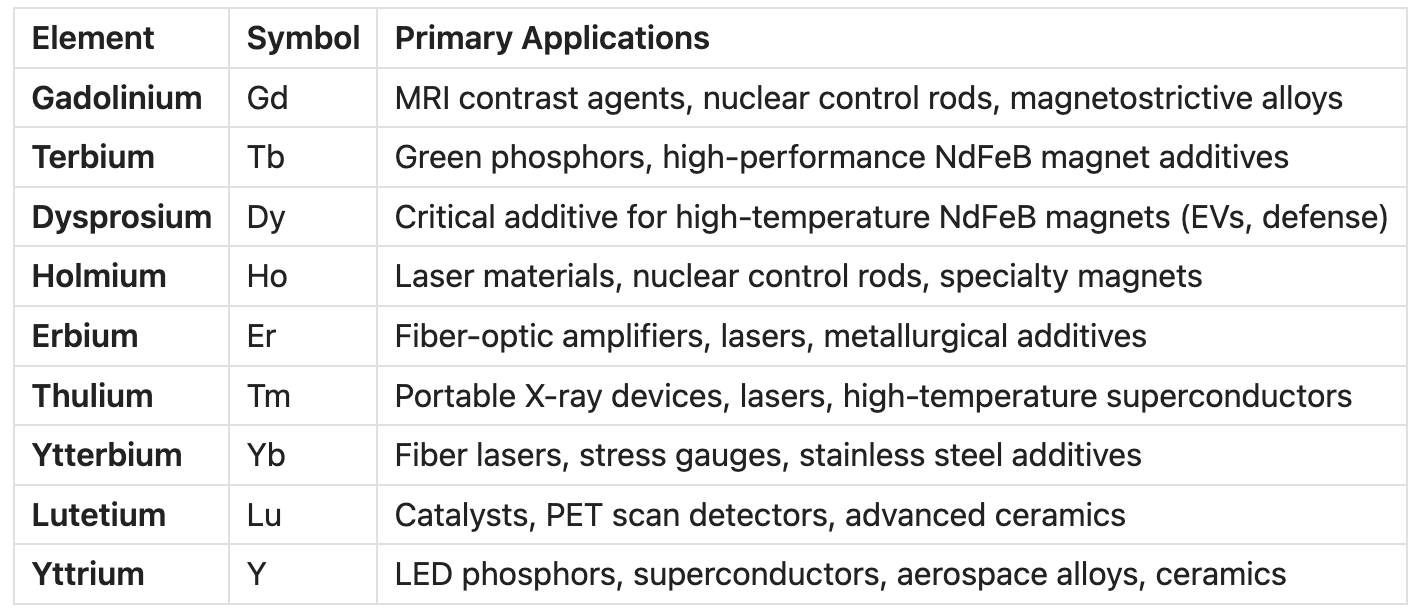

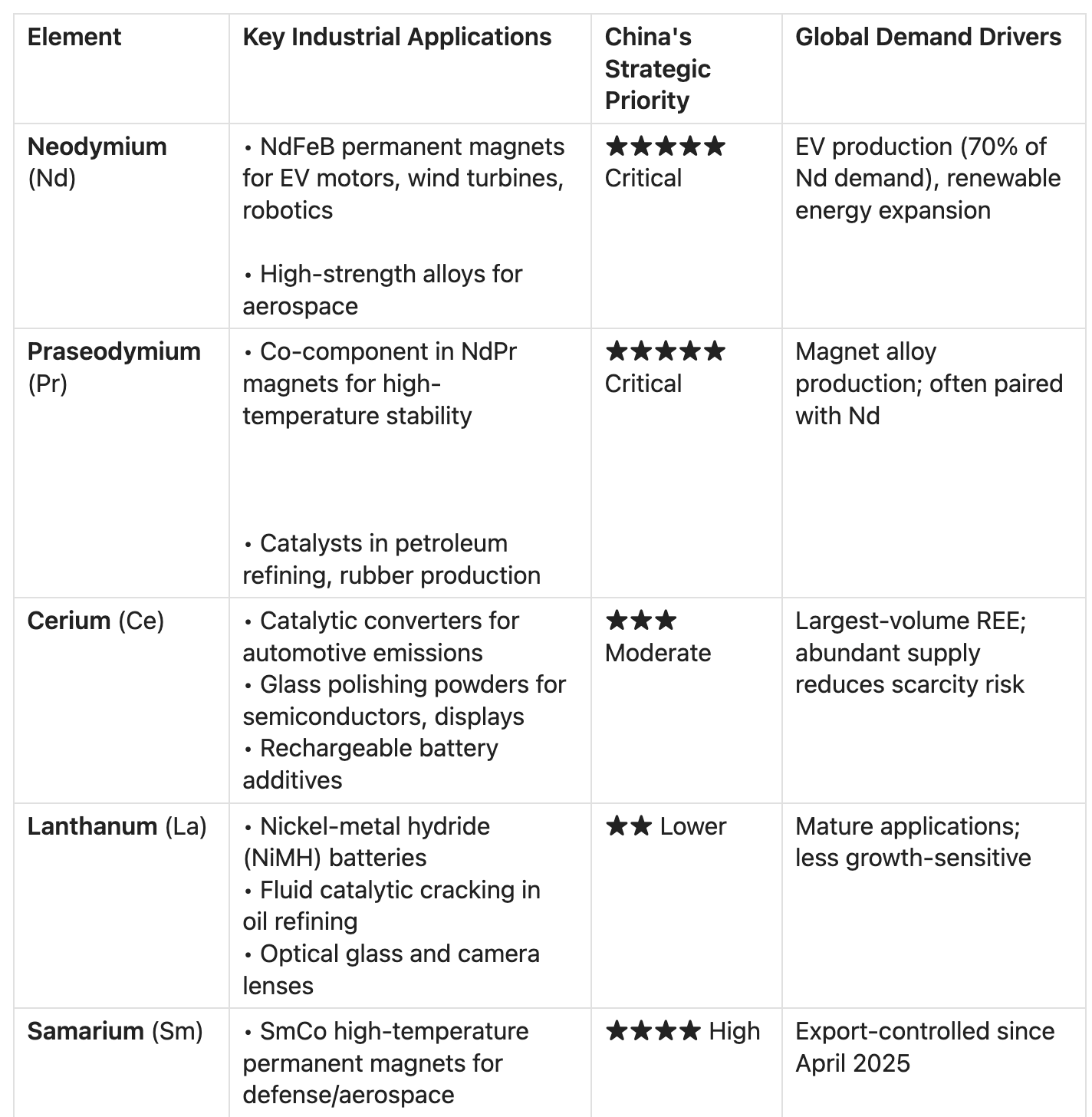

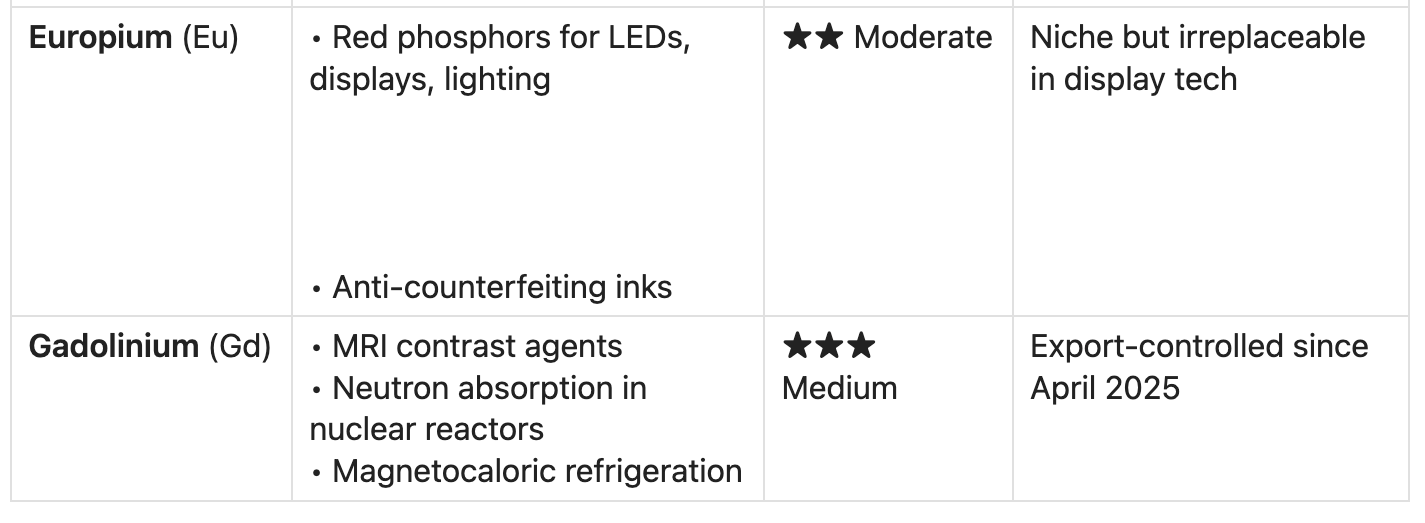

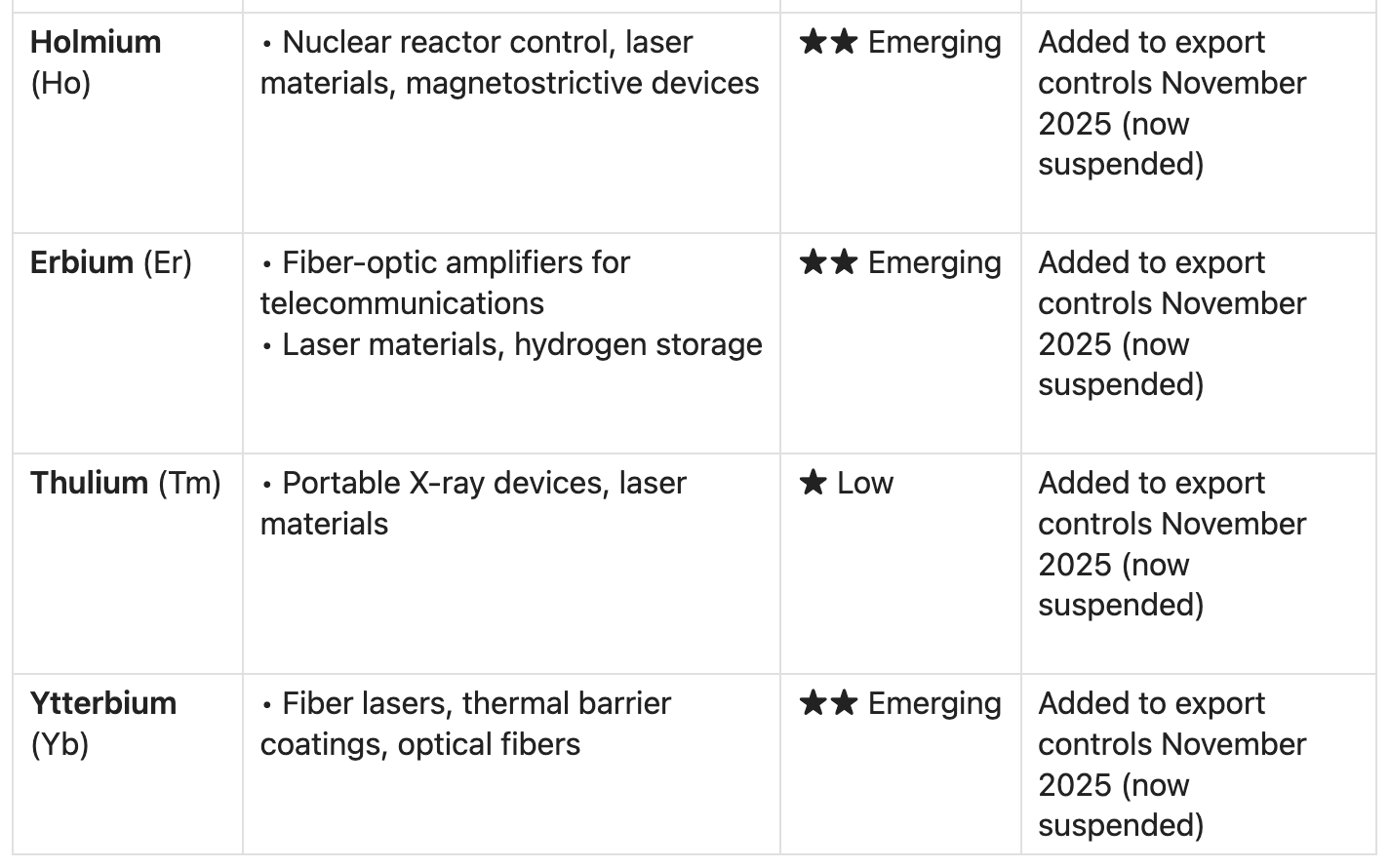

Key Light & Heavy Rare Earth Elements: Strategic Importance to China and Global Industries

Within this ecosystem the 17 rare earth elements (REEs) are divided into light (LREEs) and heavy (HREEs) categories based on atomic weight and geochemical behaviour. China's domestic industrial strategy and export policies treat these groups differently due to their distinct applications, supply concentrations, and geopolitical leverage potential.

Most Strategic REEs by Application & Importance:

Light Rare Earth Elements (LREEs)

Heavy Rare Earth Elements (HREEs):

🇨🇳 China's Domestic Prioritisation Framework

China's industrial policy distinguishes REEs not just by geology, but by strategic value:

Tier 1: Core Strategic REEs (Highest Protection)

- Nd, Pr, Dy, Tb: Essential for permanent magnets powering China's EV, wind, and defence industries

- Managed through strict production quotas, export licensing, and domestic value-chain mandates

- China consumes ~70% of its NdPr output domestically to support its own manufacturing base

Tier 2: Controlled Leverage REEs

- Sm, Gd, Y, Sc, Lu: Used in defence, aerospace, and high-tech applications

- Subject to export licensing and "dual-use" restrictions under the 2024 Rare Earth Management Regulations

- Export controls enable geopolitical signalling while preserving domestic supply

Tier 3: Commercial Volume REEs

- Ce, La, Eu: Abundant, lower-margin applications (polishing, catalysts, lighting)

- More freely traded but still monitored under quota system

- Used to maintain market share and pricing influence globally

Global Industry Dependence by Sector:

Electric Vehicles & Clean Energy:

Critical REEs: Nd, Pr, Dy, Tb

• EV traction motors: 1–3 kg NdFeB magnets per vehicle

• Direct-drive wind turbines: 500–1,000 kg magnets per MW capacity

• Dy/Tb additives enable magnets to operate at 150–200°C without demagnetising.

China supplies ~94% of global sintered NdFeB magnet production, creating concentrated supply risk for Western automakers and turbine OEMs.

Defence & Aerospace;

Critical REEs: Sm, Dy, Tb, Y, Sc, Gd

• Precision-guided munitions: SmCo magnets for actuators and guidance systems

• Radar/sonar: Tb-doped materials for signal processing

• Jet engines: Sc-Al alloys for high-strength, lightweight components

• Stealth coatings: REE-doped ceramics for radar absorption

Electronics & Digital Infrastructure:

Critical REEs: Eu, Tb, Y, Er, Ce • Displays: Eu (red), Tb (green) phosphors for LCD/OLED screens

• Fibre optics: Er-doped amplifiers enable long-distance data transmission

•Polishing: CeO₂ for semiconductor wafer and smartphone glass finishing

Even "magnet-free" technologies often rely on REEs for supporting components, creating hidden dependencies.

Industrial & Emerging Applications:

Critical REEs: La, Ce, Sc, Ho, Lu • Catalysts: Ce/La in petroleum refining, automotive exhaust treatment

• Hydrogen economy: Sc in solid oxide fuel cells; Ho in magnetic refrigeration

•Quantum technologies: Lu, Yb in qubit research and precision sensors

The technical analysis continues on starting with the upstream sector if you want to purchase the complete report which includes the in depth analysis of the upstream, midstream, downstream, policy & regulatory environment and, logistics and shipping email me at: luqman@tycovin.com